Managing your money sometimes feels like trying to solve a tricky math puzzle, doesn’t it? There is so much financial jargon, like “stocks,” “mutual funds,” and “inflation,” that you quickly get lost. But how about managing your money as fun as slicing a pizza?

In fact, that is what the 50 30 20 rule does. It is a simple blueprint that helps you split your monthly earnings into three. When you use this rule, you can hassle-free make an excellent investment plan and still enjoy the things you love today.

Here is how this rule works and how to use it to get yourself financially free.

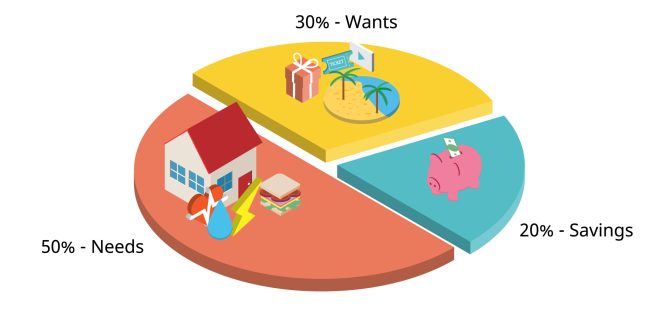

What is the 50-30-20 Rule?

Imagine your monthly income as 100%.

The rule advises you to allocate this money in three separate money pots:

- 50% for Needs: Money that pays for the basic things you need to live.

- 30% for Wants: Money for nice-to-have things.

- 20% for Savings and Investments: Money that you will use in the future.

Next, let’s look at each money pot and see how they fit into your life.

Bucket 1: The 50% for Your “Needs”

Half of your income should be allocated to the essentials that make your life comfortable and secure. In India, these usually refer to the small, unstoppable monthly expenses that you do not have unless you live a cloistered life.

The things in this bucket are:

- Housing rent or home loan installments (EMIs)

- Basic food items and milk

- Children’s tuition fees

- Bills for electricity, water, and internet

- General doctor visits and medicine

If your monthly earnings are ₹50,000, then half of it, i.e., ₹25,000, is utilized for these essential requirements. In case your essentials consume more than 50% of your income, you should think about whether partial cuts can be made. Perhaps you can find a house at a lower rent or spend less electricity.

Bucket 2: The 30% for Your “Wants”

Here’s some good news! Most people misunderstand saving money as depriving oneself of all pleasures. However, this rule is precisely telling you to spend on your joy!

These are some examples of items in this bucket:

- Dinner out or ordering food from outside

- Movies or paying for video streaming services

- Clothing that isn’t a simple school uniform

- Weekend trips with friends/family

- Buying just for the appealing camera of the new smartphone

Consider if you are making ₹50,000 a month. Then, you have ₹15,000 as per this 30% rule, which you can splurge towards your whims. The secret lies in being truthful. A mobile phone is a want and not a need, simply; that is, a lavish dinner is also a want. Only if you do not get out of your 30% commitment can you spend this money guiltlessly.

Bucket 3: The 20% for Your Future (The Investment Plan)

This is the last and most important bucket that you should allocate 20% of your income. These 20% are not just money to hide under your mattress. Actually, they are the starting capital of your investment plan. On a ₹50, 000 monthly salary, this translates into committing ₹10, 000 for your investment every month.

Why do we need an investment plan rather than just saving cash? Because of a phenomenon called inflation. In a nutshell, the cost of items like vegetables, petrol, and clothes increases every year. If you continue to keep your money in a plain box or a basic bank savings account, its purchasing power gradually decreases. Investing is one of the ways to ensure that the value of your money outgrows that of rising prices.

How to Use Your 20% to Build and Execute a Sound Investment Plan

To those who are not familiar with investing, the financial world might seem daunting and scary. And nonetheless, you must not feel discouraged from continuing. You may even be that one step away from a huge success. Moreover, you may begin something really small. These are simple instructions to implement the 20% properly:

1. Create a Safety Net

Stock purchase should come only after you throw your first few months of savings in an emergency fund. This is a stash of money that you, in fact, should not be using if nothing goes amiss, such as a sudden illness or becoming unemployed. You may keep money equivalent to your six-month expenditures in a very safe and quite liquid bank account.

2. Open a Public Provident Fund (PPF)

The PPF is one of the best ways to save money safely in India. It has a government guarantee, the interest rate is good, and there is an income tax benefit. It is suitable mainly for very long-term objectives such as child education or retirement.

3. Use Mutual Funds via SIP

An SIP is short for Systematic Investment Plan, which is basically a tool wherein you commit a fixed sum of money every month to investing in the market. The system will just debit the agreed amount from your account on its own and invest it in your chosen scheme. You don’t need tens of thousands to start investing in the market through an SIP you can begin with a mere ₹500 monthly.

As the years pass, even the tiniest deposits can result in a substantial capital accumulation due to the magic of compounding. (Compounding denotes that not only does your principal earn interest, but the accumulated interest also earns interest over time.)

4. Gold and Fixed Deposits (FDs)

It’s no secret that in India, we have an affinity for gold and fixed deposits (FDs). They are the go-to investment options mainly because they are reliable and safe over time. A limited share of your 20% allocation can be invested here to enjoy short-term safety and peace of mind.

Why This Rule Works Perfectly in India

While older generations may sometimes be keen on saving every single rupee, younger generations look forward to spending on experiences that they remember. That is why the 50/30/20 rule works well as a win-win solution for both these mutually exclusive lifestyles. It inculcates balance in us; it not only curbs our overconsumption but also makes sure that we are not confined by saving habits that are too extreme.

Whether you are a 22-year-old who has just gotten a job in Bengaluru and is still trying to get used to the work routine or a 45-year-old housewife who’s been managing a household up till now, the percentages would be the same for both of you.

Conclusion: Just Start With What You Have

It is not necessary to have a lot of money before you can begin an investment plan. What you actually need is a method. The 50 30 20 rule will provide you with such a method.

On the other hand, if allocating 20% appears to be a stretch now due to your expenses, there’s no need for that. You can even start with 5% or 10%. It is more about the investment habit that you develop over time rather than the actual figure. As your earnings increase with time, your ability to save can also gradually improve.

The actions that you decide to undertake today will get your future self thanking you. Allow yourself to fulfill your desires, but at the same time, protect your savings so that you are also smart to your future self.